45. Job Search IV: Correlated Wage Offers#

In addition to what’s in Anaconda, this lecture will need the following libraries:

!pip install quantecon jax

45.1. Overview#

In this lecture we solve a McCall style job search model with persistent and transitory components to wages.

In other words, we relax the unrealistic assumption that randomness in wages is independent over time.

At the same time, we will go back to assuming that jobs are permanent and no separation occurs.

This is to keep the model relatively simple as we study the impact of correlation.

We will use the following imports:

import matplotlib.pyplot as plt

import jax

import jax.numpy as jnp

import jax.random as jr

import quantecon as qe

from typing import NamedTuple

45.2. The model#

Wages at each point in time are given by

where

Here \(\{ \zeta_t \}\) and \(\{ \epsilon_t \}\) are both IID and standard normal.

Here \(\{y_t\}\) is a transitory component and \(\{z_t\}\) is persistent.

As before, the worker can either

accept an offer and work permanently at that wage, or

take unemployment compensation \(c\) and wait till next period.

The value function satisfies the Bellman equation

In this expression, \(u\) is a utility function and \(\mathbb E_z\) is expectation of next period variables given current \(z\).

The variable \(z\) enters as a state in the Bellman equation because its current value helps predict future wages.

45.2.1. A simplification#

There is a way that we can reduce dimensionality in this problem, which greatly accelerates computation.

To start, let \(f^*\) be the continuation value function, defined by

The Bellman equation can now be written

Combining the last two expressions, we see that the continuation value function satisfies

We’ll solve this functional equation for \(f^*\) by introducing the operator

By construction, \(f^*\) is a fixed point of \(Q\), in the sense that \(Q f^* = f^*\).

Under mild assumptions, it can be shown that \(Q\) is a contraction mapping over a suitable space of continuous functions on \(\mathbb R\).

By Banach’s contraction mapping theorem, this means that \(f^*\) is the unique fixed point and we can calculate it by iterating with \(Q\) from any reasonable initial condition.

Once we have \(f^*\), we can solve the search problem by stopping when the reward for accepting exceeds the continuation value, or

For utility we take \(u(c) = \ln(c)\).

The reservation wage is the wage where equality holds in the last expression.

That is,

Our main aim is to solve for the reservation rule and study its properties and implications.

45.3. Implementation#

Let \(f\) be our initial guess of \(f^*\).

When we iterate, we use the fitted value function iteration algorithm.

In particular, \(f\) and all subsequent iterates are stored as a vector of values on a grid.

These points are interpolated into a function as required, using piecewise linear interpolation.

The integral in the definition of \(Qf\) is calculated by Monte Carlo.

Here’s a NamedTuple that stores the model parameters and data.

Default parameter values are embedded in the model.

class JobSearchModel(NamedTuple):

μ: float # transient shock log mean

s: float # transient shock log variance

d: float # shift coefficient of persistent state

ρ: float # correlation coefficient of persistent state

σ: float # state volatility

β: float # discount factor

c: float # unemployment compensation

z_grid: jnp.ndarray

e_draws: jnp.ndarray

def create_job_search_model(μ=0.0, s=1.0, d=0.0, ρ=0.9, σ=0.1, β=0.98, c=5.0,

mc_size=1000, grid_size=100, key=jr.PRNGKey(1234)):

"""

Create a JobSearchModel with computed grid and draws.

"""

# Set up grid

z_mean = d / (1 - ρ)

z_sd = σ / jnp.sqrt(1 - ρ**2)

k = 3 # std devs from mean

a, b = z_mean - k * z_sd, z_mean + k * z_sd

z_grid = jnp.linspace(a, b, grid_size)

# Draw and store shocks

e_draws = jr.normal(key, (2, mc_size))

return JobSearchModel(μ=μ, s=s, d=d, ρ=ρ, σ=σ, β=β, c=c,

z_grid=z_grid, e_draws=e_draws)

Next we implement the \(Q\) operator.

@jax.jit

def Q(model, f_in):

"""

Apply the operator Q.

* model is an instance of JobSearchModel

* f_in is an array that represents f

* returns Qf

"""

μ, s, d = model.μ, model.s, model.d

ρ, σ, β, c = model.ρ, model.σ, model.β, model.c

z_grid, e_draws = model.z_grid, model.e_draws

M = e_draws.shape[1]

def compute_expectation(z):

def evaluate_shock(e):

e1, e2 = e[0], e[1]

z_next = d + ρ * z + σ * e1

go_val = jnp.interp(z_next, z_grid, f_in) # f(z')

y_next = jnp.exp(μ + s * e2) # y' draw

w_next = jnp.exp(z_next) + y_next # w' draw

stop_val = jnp.log(w_next) / (1 - β)

return jnp.maximum(stop_val, go_val)

expectations = jax.vmap(evaluate_shock)(e_draws.T)

return jnp.mean(expectations)

expectations = jax.vmap(compute_expectation)(z_grid)

f_out = jnp.log(c) + β * expectations

return f_out

Here’s a function to compute an approximation to the fixed point of \(Q\).

@jax.jit

def compute_fixed_point(model, tol=1e-4, max_iter=1000):

"""

Compute an approximation to the fixed point of Q.

"""

def cond_fun(state):

f, i, error = state

return jnp.logical_and(error > tol, i < max_iter)

def body_fun(state):

f, i, error = state

f_new = Q(model, f)

error_new = jnp.max(jnp.abs(f_new - f))

return f_new, i + 1, error_new

# Initial state

f_init = jnp.full(len(model.z_grid), jnp.log(model.c))

init_state = (f_init, 0, tol + 1)

# Run iteration

f_final, iterations, final_error = jax.lax.while_loop(

cond_fun, body_fun, init_state)

return f_final

Let’s try generating an instance and solving the model.

model = create_job_search_model()

with qe.Timer():

f_star = compute_fixed_point(model).block_until_ready()

0.42 seconds elapsed

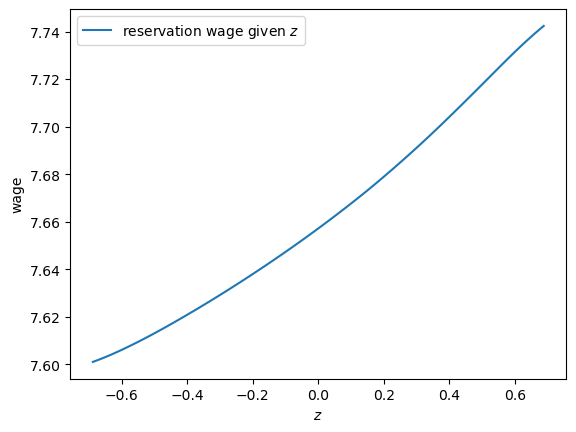

Next we will compute and plot the reservation wage function defined in (45.1).

res_wage_function = jnp.exp(f_star * (1 - model.β))

fig, ax = plt.subplots()

ax.plot(model.z_grid, res_wage_function,

label="reservation wage given $z$")

ax.set(xlabel="$z$", ylabel="wage")

ax.legend()

plt.show()

Notice that the reservation wage is increasing in the current state \(z\).

This is because a higher state leads the agent to predict higher future wages, increasing the option value of waiting.

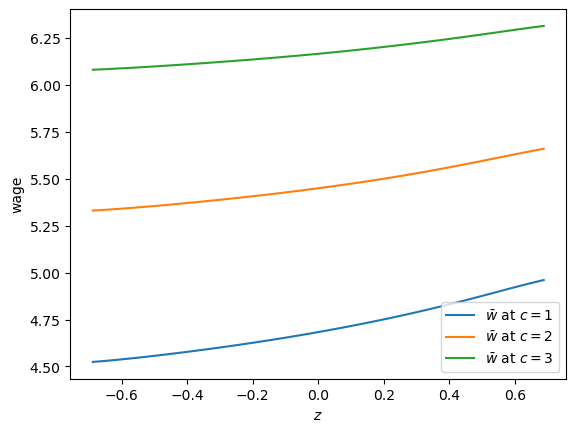

Let’s try changing unemployment compensation and look at its impact on the reservation wage:

c_vals = 1, 2, 3

fig, ax = plt.subplots()

for c in c_vals:

model = create_job_search_model(c=c)

f_star = compute_fixed_point(model)

res_wage_function = jnp.exp(f_star * (1 - model.β))

ax.plot(model.z_grid, res_wage_function,

label=rf"$\bar w$ at $c = {c}$")

ax.set(xlabel="$z$", ylabel="wage")

ax.legend()

plt.show()

As expected, higher unemployment compensation shifts the reservation wage up at all state values.

45.4. Unemployment duration#

Next we study how mean unemployment duration varies with unemployment compensation.

For simplicity we’ll fix the initial state at \(z_t = 0\).

def compute_unemployment_duration(model,

key=jr.PRNGKey(1234), num_reps=100_000):

"""

Compute expected unemployment duration.

"""

f_star = compute_fixed_point(model)

μ, s, d = model.μ, model.s, model.d

ρ, σ, β, c = model.ρ, model.σ, model.β, model.c

z_grid = model.z_grid

@jax.jit

def f_star_function(z):

return jnp.interp(z, z_grid, f_star)

@jax.jit

def draw_τ(key, t_max=10_000):

def cond_fun(state):

z, t, unemployed, key = state

return jnp.logical_and(unemployed, t < t_max)

def body_fun(state):

z, t, unemployed, key = state

key1, key2, key = jr.split(key, 3)

# Draw current wage

y = jnp.exp(μ + s * jr.normal(key1))

w = jnp.exp(z) + y

res_wage = jnp.exp(f_star_function(z) * (1 - β))

# Check if optimal to stop

accept = w >= res_wage

τ = jnp.where(accept, t, t_max)

# Update state if not accepting

z_new = jnp.where(accept, z,

ρ * z + d + σ * jr.normal(key2))

t_new = t + 1

unemployed_new = jnp.logical_not(accept)

return z_new, t_new, unemployed_new, key

# Initial state: (z, t, unemployed, key)

init_state = (0.0, 0, True, key)

z_final, t_final, unemployed_final, _ = jax.lax.while_loop(

cond_fun, body_fun, init_state)

# Return final time if job found, otherwise t_max

return jnp.where(unemployed_final, t_max, t_final)

# Generate keys for all simulations

keys = jr.split(key, num_reps)

# Vectorize over simulations

τ_vals = jax.vmap(draw_τ)(keys)

return jnp.mean(τ_vals)

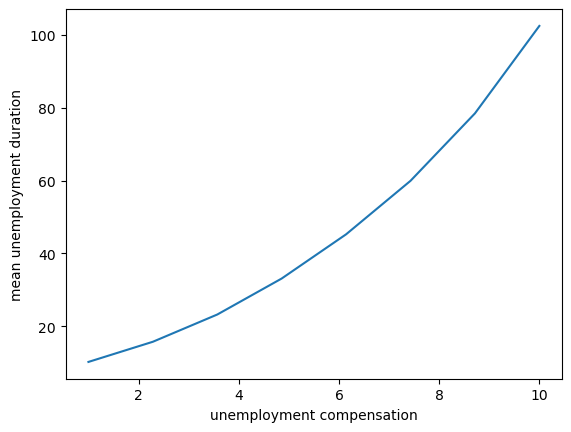

Let’s test this out with some possible values for unemployment compensation.

c_vals = jnp.linspace(1.0, 10.0, 8)

durations = []

for i, c in enumerate(c_vals):

model = create_job_search_model(c=c)

τ = compute_unemployment_duration(model, num_reps=10_000)

durations.append(τ)

durations = jnp.array(durations)

Here is a plot of the results.

fig, ax = plt.subplots()

ax.plot(c_vals, durations)

ax.set_xlabel("unemployment compensation")

ax.set_ylabel("mean unemployment duration")

plt.show()

Not surprisingly, unemployment duration increases when unemployment compensation is higher.

This is because the value of waiting increases with unemployment compensation.

45.5. Exercises#

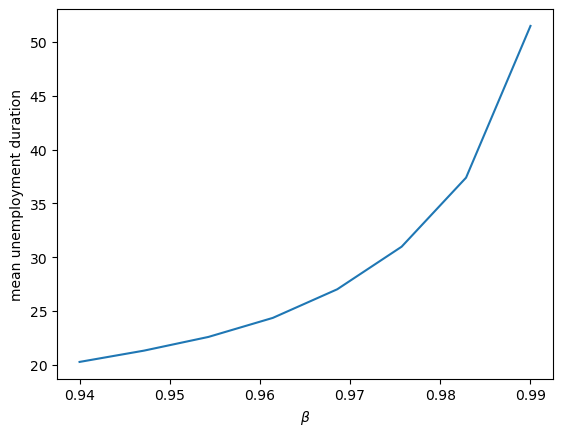

Exercise 45.1

Investigate how mean unemployment duration varies with the discount factor \(\beta\).

What is your prior expectation?

Do your results match up?

Solution to Exercise 45.1

Here is one solution

beta_vals = jnp.linspace(0.94, 0.99, 8)

durations = []

for i, β in enumerate(beta_vals):

model = create_job_search_model(β=β)

τ = compute_unemployment_duration(model, num_reps=10_000)

durations.append(τ)

durations = jnp.array(durations)

fig, ax = plt.subplots()

ax.plot(beta_vals, durations)

ax.set_xlabel(r"$\beta$")

ax.set_ylabel("mean unemployment duration")

plt.show()

The figure shows that more patient individuals tend to wait longer before accepting an offer.